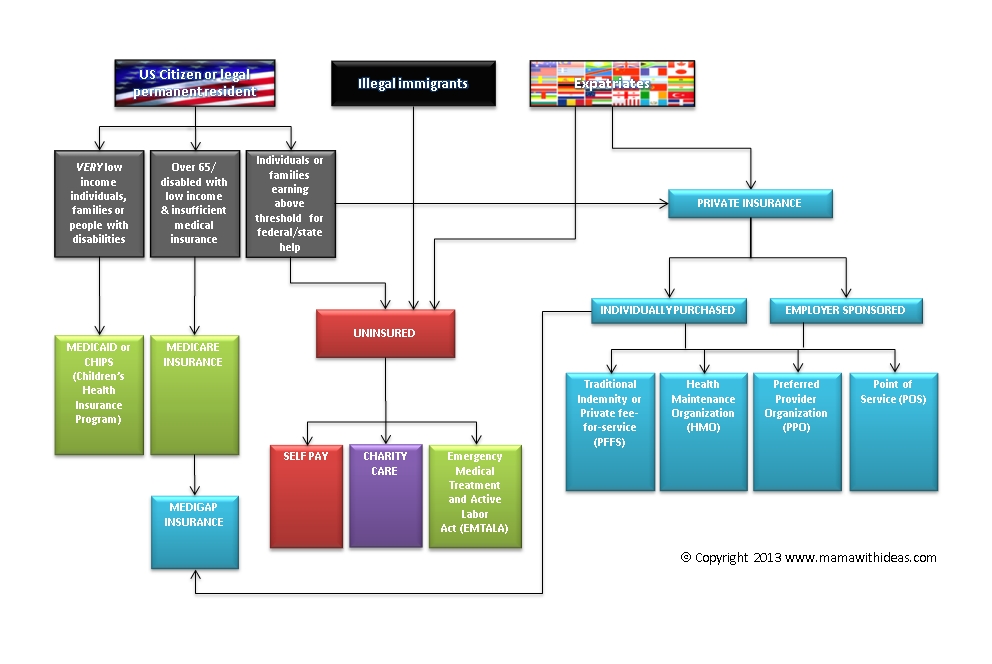

While this series is aimed at explaining the US medical care system to expats, I am going to start by giving a brief overview of the government funded insurance programs that exist to support US citizens and legal permanent residents with low incomes. The reason for this is that I was utterly bamboozled by the names being bandied around when I first encountered a healthcare provider in America and so I think it is helpful to get the broader picture.

Back in 2010 when we were relocating to the US from the UK, one of our 18 month old twins ended up with a high fever on the flight from London Heathrow to Houston. Talk about bad timing! A few days later and he had developed a blotchy rash across his torso and I was starting to worry. In the UK, I would probably have called the nurse at our local GPs office for some reassurance, but in an unfamiliar environment and without a regular medical provider I panicked a bit. We called my husband's employer who put us in touch with our employer-sponsored medical insurer to find out what to do... at this point they hadn't even issued us with our policy details! Thankfully, they emailed me details of a paediatrician not too far from our temporary accommodation and I took the Shouty One to get checked out.

This was my first encounter with the forms you have to complete when visiting a healthcare provider in the US. I was surprised they didn't want to know my inseam length and favourite colour on top of all the other information!!! Unfortunately, being in the country for less than 3 days I was still jet lagged and had no idea what most of the questions were about. I didn't have a permanent address, US telephone number and had no idea what SSN# and DL# stood for (social security number and driving licence number, not that I had obtained either at the time)! And I must have looked like a right prat when I asked the receptionist whether she knew if I had Medicaid?

So, even though it probably doesn't apply to most of you reading this article, I

AM going to give a quick summary of all types of insurance, including those funded by state and federal government for some US citizens!

NOTE: A glossary of terms is at the bottom of this post.

Another caveat: please remember that this is a high-level overview. Check the details of your own medical policy carefully as every one is different and specific things may or may not be covered by your own policy.

A - MEDICAID, CHIPS, MEDICARE & MEDIGAP...

Medicaid

Medicaid is a means-tested federal and state funded insurance program. It was expanded in 2010 by the Affordable Care Act (nicknamed "Obamacare") to include individuals and families with incomes under 133% of the poverty threshold. In 2011, this was $29,700 annual income for a family of four. Medicaid beneficiaries receive free treatment for a limited number of healthcare services, but in some states people are required to pay a small co-payment (a set fee collected at time of treatment by the healthcare provider).

CHIPS (Children's Health Insurance Programs) is a supplementary program that provides healthcare to uninsured children under the age of 19 who come from low-income families that don't qualify for Medicaid.

Medicare is also a means-tested state funded plan but it's aim is to assist low-income individuals over the age of 65 and people that are disabled and unable to work. It provides Hospital Insurance (part A) for eligible individuals and covers limited costs incurred by patients requiring hospitalisation as an in-patient... assuming they paid FICA tax (similar to National Insurance contributions in UK) for at least 10 years. Additional coverage must be paid for by the individual if they need Medical Insurance (Part B), e.g. to see a doctor/GP. Further coverage can be purchased to cover extra costs (Part C) & prescriptions (Part D).

Medigap insurance is private insurance that can be purchased by individuals to supplement Medicare.

B - Private Medical Insurance

60% of people in the US participate in an employer sponsored health insurance scheme. This type of insurance is paid for in whole, or in part, by businesses on behalf of their employees as part of an employee benefit package. Although workers are effectively paid less than they would be (because of the cost of insurance premiums to the employer), this type of insurance offers several benefits to workers, notably economies of scale, whereby they qualify for group discounts.

Only 9% of people in the US have individual health insurance that they have purchased directly from the insurer. In this case, the individual pays the entire premium without benefit of an employer contribution. In general, overall out-of-pocket costs for these types of plans are higher than employer-sponsored schemes.

There are many different types of policies, both employer-sponsored and individually purchased. Below is a summary of some of the common types:

1. Traditional Indemnity (sometimes called Private Fee-For-Service, PFFS)

This is the most basic type of healthcare insurance available, whereby beneficiaries pay a monthly premium and can submit receipts for their medical expenses to their insurer for re-imbursement, as long as they are services specifically covered by the policy.

2. HMO (Health Maintenance Organization)

HMOs were historically called pre-paid Health Plans and are still sometimes referred to as these. Key features of an HMO plan:

- Patients are required to choose a primary care physician (PCP), like a GP in the UK. Women can select to have an OB/GYN as their PCP. The PCP will take care of most of an individuals healthcare needs.

- If the individual needs to see a specialist, they must obtain a referral from their PCP first. HMO policies also require beneficiaries to only see approved (in-network) health care providers.

- Expenses usually include the monthly insurance premiums and co-payments (a fixed dollar amount paid every time an individual sees a physician or buys a prescription). The co-payment is paid at the time of service directly to the provider and no further payments required. This is particularly beneficial to expectant mothers whose policy covers maternity services. They often only have to pay a co-pay at their first doctors visit and then all subsequent care during the pregnancy is covered.

- HMOs often provide preventive care for a lower co-pay or for free, in order to keep members from developing a preventable condition that would require a great deal of medical services, e.g. immunisations, well-baby checkups, mammograms etc...

- Experimental treatments and elective services that are not medically necessary (such as elective plastic surgery) are almost never covered.

3. Preferred Provider Organization (PPO)

In the case of a PPO policy, enrollees are encouraged to seek healthcare services from certain 'preferred' healthcare providers that have a negotiated discount with the insurance company. Key features:

- Patients have greater flexibility. They do not have to enroll with a Primary Care Physician and do not require a referral from a PCP in order to see a specialist. They can chose to visit ANY healthcare provider they like rather than just those on an approved list.

- Most PPO policies have a deductible. This is the amount of expenses that must be paid out of pocket before an insurer will pay any expenses. In the UK this is called an excess. Deductibles are typically used to deter enrollees claiming for trivial items. Policy holders are required to pay 100% of all medical expenses they incur until they reach the set deductible for their policy. Some policies have cumulative family deductibles.

- Expenses usually include the monthly insurance premiums, the deductible and a co-insurance amount (a percentage of the cost, shared with the insurer).

- The co-insurance amount varies dependent on whether the patient has chosen to see a provider that is in-network or out-of-network. For example, if a patient visits an in-network doctor's and the total bill is $100, they may be required to pay a 20% coinsurance (they will pay the doctor $20 and the insurer will pay the doctor $80). For out-of-network doctors there may be a 40%/60% split instead. This encourages policy enrollees to seek in-network providers only.

- Some healthcare providers will expect the deductible and/or coinsurance to be paid at the time of service. In this case the patient will be given an itemised invoice and receipt. Other healthcare providers may send a bill for the deductible and/or coinsurance at a later date. In both cases, the insurance company will send a statement (for information only) to the patient reflecting these payments.

- Some in-network providers will charge a co-payment instead of the coinsurance for certain limited services on a PPO plan. For example, a 'Wellness Check' (annual health screening for preventative purposes) or an Emergency Room visit may be included on the policy as a service that carries a set co-payment amount. In the case of both of these, if any 'treatment' or 'service' is required, the patient will usually also be responsible for the deductible/coinsurance. For example, a friend of mine attended a Well Woman checkup (covered by a co-pay on her policy). At the end of the appointment, the Doctor asked if she had any questions and she asked about a health issue of concern. As this was an issue not strictly covered by the Well Woman Check-up, she was billed for a doctor's visit in addition to the co-pay!

- PPOs have a set out-of-pocket maximum. This is a cap or limit on the amount that an individual will have to spend in any plan year. Due to the variability in out‐of‐pockets costs on a PPO plan, out‐of‐pocket maximums help PPO members gauge the total they will pay in any one plan year. Once the out-of-pocket maximum has been reached, the insurance company will pay 100% of the cost of medical services. The maximums are usually higher for out‐of‐network services and the maximums do not cross accumulate.

3. Point of Service (POS)

A point of service plan, or POS plan, combines characteristics of traditional indemnity, HMO and PPO plans.

- Individuals with a POS plan only choose which system to use at the time of service. Like an HMO plan, a POS gives lower medical costs in exchange for more limited choice. However, the flexibility of a PPO is there if the patient requires it.

- A patient with a POS plan is required to choose an in-network primary care physician to monitor their health care and to be their "point of service". However, unlike with a traditional HMO, the primary POS physician may then make referrals outside the network if the patient requests it. However, the patient will only receive partial reimbursement by the health insurance company if they choose to take this route.

- For medical visits within the health care network, a co-payment and/or coinsurance is collected and the paperwork is completed for the patient. If the patient chooses to obtain a referral outside the network, it is the patient's responsibility to fill out the forms, send bills in for payment, and keep an accurate account of health care receipts.

----------------------------

I hope the overview of policy types has been helpful. Please see the other posts in this series for more information.

PART 1: An Expats Guide to Understanding the US Medical System ... an Overview

This article gives an overview of the US Medical System as summarised by this flow diagram.

And coming soon...

PART 3: An Expats Guide to Understanding the US Medical System ... Where to go for healthcare

PART 4: An Expats Guide to Understanding the US Medical System ... Paying the bill

----------------------------

GLOSSARY OF TERMS

CO-PAYMENT (a.k.a. CO-PAY) - A fixed-dollar amount that is paid at the time a health service or treatment is received.

CO-INSURANCE - A percentage of the cost of care that the patient is responsible for paying. For example, if a doctor's visit is $100 and you have a 20% coinsurance, you will pay the doctor $20 and your health plan will pay the doctor $80.

DEDUCTIBLE - A set amount that the patient is responsible for paying before the insurance benefits begin. An excess. For example, if you have a $1000 deductible, you are responsible for paying out $1000 from your pocket before the insurance will start paying for your health services.

IN-NETWORK - Refers to providers or health care facilities with whom the insurance company has negotiated a discount. Insured individuals usually pay less when using an in-network provider, because those networks provide services at lower cost to the insurance companies with which they have contracts. Services by out-of-network providers may not be covered, or covered only in part by an individual’s insurance company.

OUT-OF-POCKET MAXIMUM - A predetermined limited amount of money that an individual must pay out of their own pocket, before an insurance company will pay 100%of the individual's health care expenses.

PRIMARY CARE PHYSICIAN (PCP) - A health care professional (usually a physician) who is responsible for monitoring an individual’s overall health care needs. Like a GP.